While setting goals is an important element in your overall financial plan, so is having a financial safety net. Whether you are aiming to save more, spend less or reduce debt this year, your best-laid plans could fall in a heap if you are not prepared for financial setbacks or unanticipated costs.

Putting a financial safety net in place does not come down to any single measure. Rather, it’s a comprehensive approach to risk that’s designed to protect you and your family’s financial wellbeing, come what may.

Build an emergency fund

The first line of financial defence for households is to have some money tucked away in a ‘rainy day’ fund for emergencies and unexpected costs. If you are living from one pay day to the next and your hot water heater bursts or your car needs urgent repairs, the temptation is to borrow money.

Indeed, that was the finding of a survey for National Australia Bank.i When faced with an unexpected cost, 40 per cent of people surveyed pulled out a credit card while 16 per cent sold personal possessions.

Credit cards are an expensive form of borrowing. If you are only able to make the minimum monthly repayment you could be paying off that hot water heater for years to come. Whereas paying cash will save you money and make your financial goals that much easier to achieve.

It’s a good idea to keep your emergency cash in a separate account where it is readily accessible but won’t get mixed up with your everyday money.

Most experts suggest you aim to put aside three to six months’ living expenses. This can take a while to build up so one time-honoured strategy is to ‘pay yourself first’. Set up a direct debit from your primary bank account to divert part of your salary each month to your emergency fund.

Reduce debt

Even with the best willpower in the world it can be difficult to put money aside for the future if you are weighed down with debt. When cash is needed for an emergency, households with high levels of debt are more likely to feel financial stress.

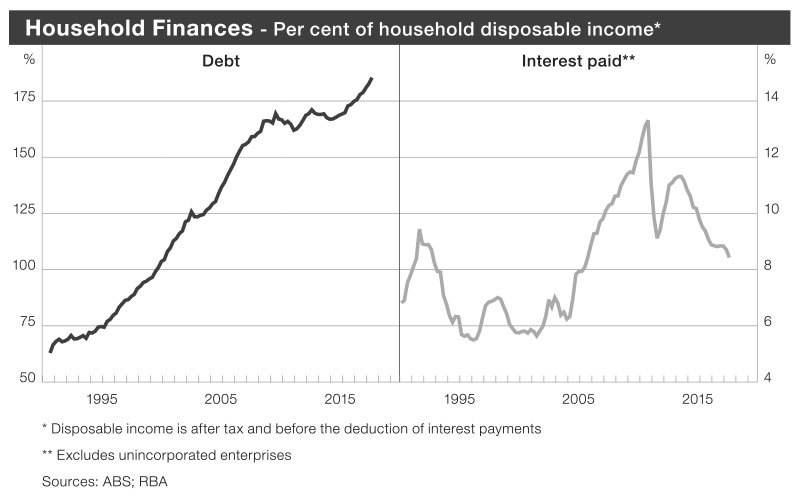

As the graph shows, the amount of debt held by Australian households as a percentage of disposable income has more than trebled over the past 25 years. By 2015 average household debt had blown out to around 185 per cent of after-tax income. While there are many reasons for this – from the rising cost of housing to student loans – there is no avoiding the conclusion that many of us are living beyond our means.

The good news is that with interest rates at or near their historic lows, there is no better time than the present to tackle debt. Aim to pay down loans with the highest interest rate first – typically this will be your credit cards.

If you have a mortgage, aim to pay more than the minimum monthly payment. By keeping at least three months ahead of schedule you can build a buffer to provide some wriggle room with your lender if you experience financial difficulties.

With home loan interest rates typically much lower than rates for personal loans and credit cards, you might consider consolidating your debts into your mortgage. Be aware though that this will effectively turn a short-term debt into one that will accrue interest for up to 30 years, so aim to step up your home loan repayments at the same time.

The price of safety is eternal vigilance, and that goes for financial safety too. So get into the habit of comparing rates for credit cards, personal loans and home loans and be prepared to switch to a different lender, where possible, if you are unable to negotiate a lower rate.

Review insurance

No financial safety net is complete without adequate personal insurance. We tend to insure our car and our house before we think about our most precious possession, our health and our ability to earn an income.

Ask yourself how your household would cope financially if you had an accident or suffered a critical illness. Worse still, what would happen if you were to die prematurely? According to the same NAB survey, a dental or medical expense was listed as the most common unexpected expense in the previous 12 months by 46 per cent of respondents.

While health insurance will cover some of your medical costs, it won’t pay the mortgage and food bills or take care of your family while you are unable to work. That’s where personal insurance comes in, to cover your life, total and permanent disability, trauma and income protection. It’s possible you already have cover for some of these through your superannuation fund, but it may not be sufficient.